This month we place the spotlight on Ultramarine & Pigments Limited (UMP), a top 3 global manufacturer of inorganic Ultramarine Blue pigment (and the leader in India and Asia-Pacific) and amongst the top manufacturer of anionic surfactants in India. Ultramarine’s pigment business enjoys significant manufacturing complexities around yield, purity and consistency particularly for industrial grade pigments. The surfactant business enjoys locational advantages since Ultramarine is the only large-scale surfactant player in south India. Helmed by technocrats, the company is focused on enhancing the product mix in both pigments (high performance pigments like Ultramarine Violet) and surfactants (specialty products for personal care) thus increasing the entry barriers. New environmental regulation is the key risk for this firm.

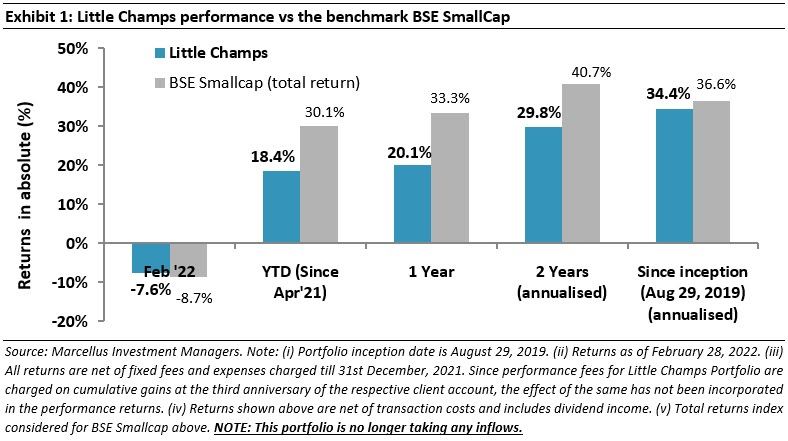

Performance update for the Little Champs Portfolio

At Marcellus, the key objective of our Little Champs Portfolio is to own a portfolio of about 15-20 sector leading franchises with a stellar track record of capital allocation, clean accounts & corporate governance and at the same time high growth potential. While we intend to fill our portfolio with winners, we want to be sure of staying away from dubious names where we are not convinced about the cleanliness of accounts or the integrity of the promoters (even though the business potential may sound promising) as the fruits of company’s performance may not get shared with minority shareholders. We intend to keep the portfolio churn low (not more than 25-30% per annum) to reap the benefits of compounding as well as minimize trading costs. The Little Champs Portfolio went live on August 29, 2019. The performance so far is shown in the below table.

Portfolio updates: Exit from Lumax Industries, addition of Paushak and Tarsons Products

We have made the following changes to portfolio in the recent months.

A. Exit from Lumax Industries

The key reasons for this exit are:

- Increased competition in the passenger vehicle automotive lighting industry particularly in the new age LED technologies. Lumax has incurred capital expenditure of close to Rs5,347 mn from FY17 to FY21. Rising competition raises concern surrounding the return on this incremental capital employed and thus the overall blended RoCE of the company.

- In light of the above, we have downgraded Lumax industries’ longevity scores and earnings growth forecast. This results in the stock sliding down the ladder in the Little Champs stock selection and position sizing framework.

B. Addition of Paushak

Paushak is the leading supplier of phosgene derivatives in India. Phosgene derivatives are some of the most basic & essential industrial chemical compounds that find application in multiple industries like pharmaceutical, agro-chemicals, personal care, etc. Owing to the highly hazardous nature of phosgene, the licensing regime in India is very stringent and this creates barriers to entry. These regulatory barriers to entry coupled with Paushak’s focus on specialty phosgene derivatives, its professional management team and continued R&D for producing more complex and value-added derivatives have enabled Paushak to grow its Revenues and PAT at ~17% CAGR and ~26% CAGR respectively for the last 10 years ending FY21 (for the 3 years ending FY21, revenue & PAT growth is 11% & 21% respectively). Paushak’s healthy growth has been accompanied by an average pre-tax ROCE of ~24% over the last 10 years (~21% average in the last 3 years).

C. Addition of Tarsons Products

Incorporated in 1983, Tarsons Products is engaged in the manufacturing of Plastic Labware Products and sells these products in India as well as in the export market (which accounts for a third of the firm’s revenues). The main customer segments for the company are research organizations, academia institutes, pharmaceutical companies, Contract Research Organizations (CROs), diagnostic companies and hospitals. Tarsons’ leadership in the Indian plastic labware market is underpinned by its in-house manufacturing capabilities and a strong distribution network. Manufacturing the product in-house has enabled the company to price its products very competitively. The precision required around manufacturing a large number of SKUs and the capital-intensive nature of the business act as high barriers to entry in the domestic market. On the other hand, the niche size of the industry (total revenues Rs12 bn) makes it unfeasible for MNC manufacturers to commence manufacturing in India. The company has grown its revenue at 13% CAGR over the last 5 years (FY16-21) and PAT at 49% CAGR with average ROCEs of 30%. With its new plant, Tarsons is expanding its capacities by more than 2x and is also expanding into new segments like Polymerase chain reaction (PCR) and Cell culture which are currently dominated by MNC players in India.

Stock in the Spotlight: Ultramarine & Pigments

This month we detail our investment rationale for Ultramarine & Pigments. In the previous months we have written on: Garware Technical Fibres (August 2020), GMM Pfaudler (September 2020), V-Mart Retail (October 2020), Alkyl Amines (November 2020), Suprajit Engineering (December 2020), Mold-Tek Packaging (February 2021), Amrutanjan (April 2021), Fine Organics (May 2021) and Galaxy Surfactants (December 2021).

Company and management background

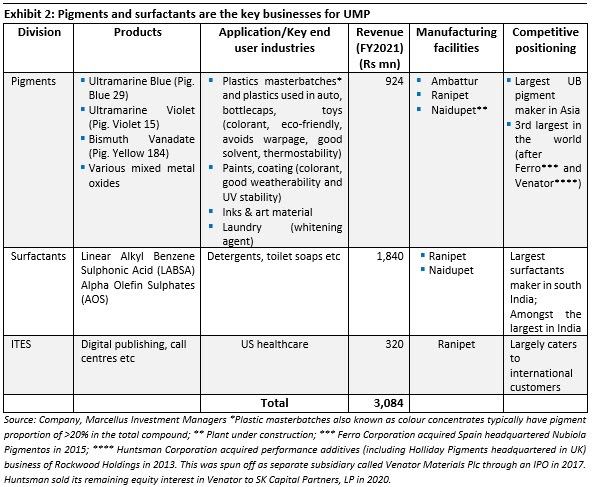

Ultramarine & Pigments Limited (UMP), incorporated in 1960 in Mumbai, started as a trading company for the Ultramarine Blue (UB) pigment. In 1962, the first unit for in-house manufacturing of UB pigment was set up in Ambattur (Chennai, Tamil Nadu) through a technical agreement with a large German chemical company. The anionic surfactants division was started in mid-1970s in Ranipet (Tamil Nadu) initially with Linear Alkyl Benzene Sulphonic Acid (LABSA), a common surfactant used for detergents. In late 1990s another anionic surfactant Alpha Olefin Sulphate (AOS) was added to the portfolio. The pigment and surfactants divisions continue to be Ultramarine’s mainstays accounting for 90% of total revenues in FY2021. Excluding ITES, 20% of the revenues come from exports (the majority from the pigments segment).

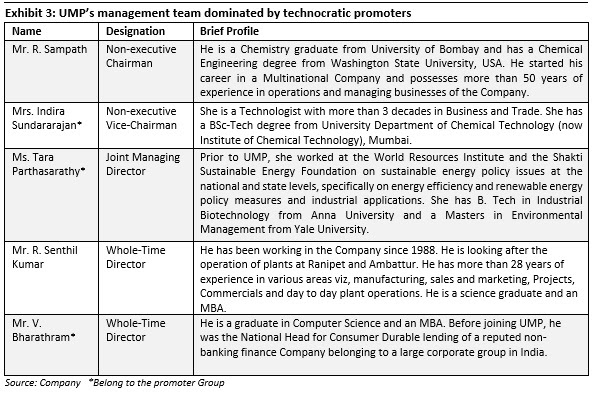

The company has historically been managed by the promoter family members. Currently the third generation of the promoter are also involved in the business.

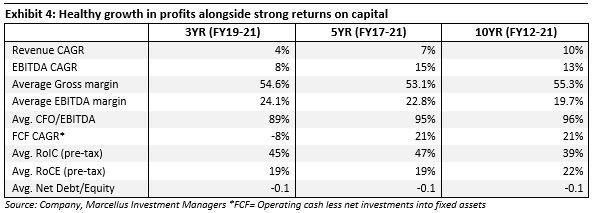

Healthy growth in profits complimented by strong returns on capitalOver the last 5/10 years (ending FY21), the Company has witnessed healthy double-digit growth in EBITDA due to improving product mix, scale benefits and operational efficiency (evaluating top-line growth may not be appropriate due to raw material pass-through impacts). Helped by healthy margins (average EBIT margin of 20.6% over FY17-21), decent net fixed assets turnover (average 3.5x over FY17-21) and modest working capital days (average 53 days over FY17-21), the company has been able to generate high RoIC (pre-tax) and free cash over the years (the most recent years impacted due to significant expansion in the surfactants capacity). However, the high RoIC (of 45%) is not fully translated into high RoCE (of 20%) as can be seen in the below exhibit due to the following reasons:

- UMP owns 19.97% equity stake in a listed group company Thirumalai Chemicals (TCL). The company marks-to-market the value of this stake as per the IND-AS requirements. As at FY21-end, TCL stake was valued at ~Rs1,750mn (35% of the UMP’s capital employed at FY21-end).

- UMP had cash of ~Rs852mn as at FY21-end (17% of capital employed) which also suppresses RoCE to a significant extent.

|

|

What we like about UMP?

A. Complexities surrounding UB pigment manufacturing mastered by only a handful of global players

Historically the usage of UB pigment was largely for laundry applications. However, over the last 2-3 decades, the UB pigment has found increasing industrial applications like plastics, paints, etc due to its functional characteristics described in exhibit 1 above.

However, pigments used in these industrial applications vs basic laundry applications differ substantially in terms in terms of parameters like strength of the colour (brightness), the level of purity (defined by content of sulphur/iron/lead/aluminium, etc) and the degree of corrosion resistance. Only three UB pigment manufacturers in the world accounts for a lion’s share of the total industrial grade UB pigment capacities and sales (while there are many players manufacturing the laundry grade UB). UMP is the third largest UB global pigment manufacturer and the largest supplier in India (meeting >60% of country’s industrial grade pigment requirements) and the Asia-Pacific.

We attribute the following reasons for a concentrated market in the industrial grade UB pigment:

Challenges surrounding yield and efficiency

A typical process manufacturing involves the following steps:

- Raw materials – China clay, Soda Ash, Sulphur, Tar pitch, etc – are mixed and are grounded into very fine particles in a dry ball mill.

- After grinding, this raw mix is filled in refractory pots and loaded in the batch kilns which are heated using fuels (typically coal, coke or LPG/LNG) to the required temperature and the temperature is maintained to particular time (this is called the calcination process).

- After this the kiln is allowed for natural cooling which takes min 25 to 30 days depending upon the atmospheric conditions.

- Then the kilns are opened to unload raw blue (Pigment + By Product) and washed in the washing tanks/equipments to remove the water-soluble salts.

- This mixture is then grinded using wet mills to get desired particle size followed by natural settling to separate the pigment based on the particle size.

A lot of variables go into the above manufacturing process such as the weather/climatic conditions surrounding the plant (which influences factors like temperature particularly during the natural cooling process), the amount and time of introducing oxygen during the calcination process, the level of heavy metals in the raw material ores etc. Any deviation in these parameters can result in significant yield drop and difference in quality across batches. Over time, only a handful of players have been able to enhance the yield by optimizing the process conditions (through automation, sophisticated instrumentation techniques etc). Also, energy is a big cost and only few players like UMP has been able to bring down the energy consumption significantly over the years.

Achieving consistency in quality across batches

UB pigments are manufactured in batches and achieving consistency in quality across different batches is a big challenge due to the variabilities mentioned in the preceding section. Furthermore, the quality of the output can be ascertained only at the end of a long manufacturing process (described above) which adds further layers of complexities. At the same time, inconsistency in quality can impact colour texture and functional properties of the final product. This also makes it difficult to switch between vendors. UMP has been successful in building consistency in quality across batches due to the processes that have been developed over decades of experience. This is an enormous source of customer stickiness for UMP.

Meeting environment and safety requirements

The UB pigment manufacturing process involves environmental implications such as generation of pollutants like Sulphur Dioxide (SO2) and Carbon Dioxide (CO2) during the calcination process and effluents like Total Dissolved Solids (TDS)/salts and Chemical Oxygen Demand (COD). This requires effective treatment and recycling process resulting in not only significant scrutiny from regulatory authorities in granting environment clearances but higher cost of capital. Both of these factors create barriers to entry. Furthermore, there are stringent requirements to prevent health hazards emanating from the above threshold presence of impurities like sulphur (in plastic masterbatches), lead (for complying with USFDA regulations surrounding cosmetics) and aluminium (in toy applications). These require significant process improvements/controls surrounding raw material specifications, chemical treatments, etc which adds to the costs.

The above factors present enormous entry barriers in the UB pigment industry.

B. Locational advantage in the Surfactants business

UMP’s surfactants facilities (Ranipet in Tamil Nadu and recently commissioned Naidupet in Andhra Pradesh) are located in South India. UMP is the only decent sized surfactants player having a manufacturing base in south India. Surfactant facilities have historically been concentrated in west India (particularly in the state of Maharashtra & Gujarat) due to proximity to the crude based raw materials (major players like Galaxy, Godrej Industries and Aarti Surfactants have plants in the states of Maharashtra, Gujarat, Madhya Pradesh). While UMP’s south Indian location is a disadvantage vis-à-vis access to raw material is concerned, it gives enormous advantages in terms of servicing the south Indian based customers (reliability in supplies and lower freights costs). This has enabled UMP not only to penetrate into MNC’s south Indian locations (P&G’s Hyderabad facility, HUL’s Puducherry) but more importantly become the surfactant supplier of choice for south Indian based FMCG players. Such a diversified customer base (not reliant on few large MNC customers) in turn has helped UMP’s bargaining power in the surfactants business and command relatively higher margins and returns compared to the peers.

C. Focus on higher value-added products

The company has demonstrated a strong track record of moving up the product curve in both the pigments as well as surfactants business.

In the UB pigment, historically the sales of the company were into lower-grade laundry applications, but now the majority of sales are towards industrial grade pigments. UMP’s annual reports consistently talk about the focus on developing higher grade pigments for industrial applications. This is also reflected in the strong growth in pigment realisation which increased @7% CAGR between FY07-17 (data available only until FY17 annual report). The company has also added high value pigments like Ultramarine Violet (for which UB pigment forms the input and requires much higher degree of purity) and Bismuth Vanadate (yellow) to the pigment portfolio. The focus on higher grade pigments has also helped UMP penetrate into the export markets in the most recent years. The new upcoming plant for pigments at Naidupet, Andhra Pradesh (housed in 100% subsidiary Ultramarine Specialty Chemicals Ltd) is expected to focus on high performance pigments.

Similarly in the surfactants business, the company has in the recent years also forayed into specialty surfactants like Sodium Lauryl Sulphate (SLS) and Sodium Lauryl Ether Sulphate (SLES) which are used in personal care products. The company new surfactants plant already commissioned in January 2021 is also intended to focus on SLES and others specialty surfactants.

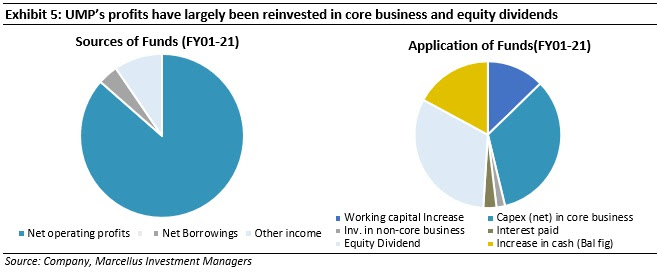

D. Capital allocation – largely into core business; non-core investments overall have been significantly value-accretive

As can be seen in the exhibit below, the company has generally followed a disciplined capital allocation policy utilising the profits mainly towards:

- Reinvestments into core businesses (pigments and surfactants) expansions and working capital; &

- Dividend distribution

|

|

However, some part of capital has historically gone into non-core businesses. These non-core forays overall have been significantly value-accretive to the company despite some investments yielding below par returns.

Successful non-core forays:

- Investment in Thirumalai Chemicals: UMP has a long-standing investment in TCL (19.97% equity stake as at December 2021-end), a listed group company. TCL (which in turn owns 13.55% equity stake in UMP as December 2021-end) is one of the world’s largest producers of Phthalic Anhydride (used to manufacture plasticizers, pigments, dyes and resins), Malic Acid (which finds applications in food and pharma products) and certain other products. Against the book value of investment of Rs132mn in TCL, the current market value (based on February 25, 2022-end share price) of UMP’s equity stake in TCL is Rs4,319 mn (49% of UMP’s February 25, 2022-end market cap) indicating significant value accretion from the TCL investment.

- IT division (part of UMP standalone): The company forayed into this business in 1999 with a focus on US healthcare business processing services, publishing and e-learning as core businesses. While the growth of this business has been muted (only Rs304mn revenue contribution in FY21), against the capital employed of Rs64mn in this business as at March 2021-end, EBIT generated was Rs93mn indicating the cash cow nature of the business.

Not so successful non-core forays:

Investment in Malaysian subsidiary of TCL: In FY01, UMP had invested Rs89.8 mn for a 19.68% equity stake in TCL Industries (Malaysia) Sdn Bhd, a JV between TCL and Yayasan Terengganu and Promet Bhd. The principal business of the company was to manufacture Maleic Anhydride (MAN) which is used in making polyester resins, Spandex fibres, etc. Malic acid, a derivative of MAN is used in artificial sweeteners and flavour enhancements. Due to high prices of its raw material– Benzene – the company made changes to its plant and started manufacturing MAN from Butane instead of Benzene from January 2008. However, due to the global meltdown in Sep-Dec 2008, TCL Malaysia had to shut down operations and accumulated huge losses. UMP wrote down the value of its investment in TCL Malaysia against the reserves in FY10.

Key Risks/concerns

- Environmental regulations: As described above, UB pigment manufacturing process involves generation of pollutants like SO2, CO2 and effluents. Strict government norms surrounding emissions (including enforcement thereof) particularly in urban areas can impact UMP. In this regard, the new plant in Naidupet is a welcome mitigation strategy.

- Shares sale by a group of Promoters: A group of Ultramarine promoters have been selling shares in the open market in the recent years. The overall promoter shareholding has come down from 52.6% as at March 2017-end to 44.5% as at December 2021-end. However, we draw somewhat comfort that shareholding of the set of promoters involved in managing the operations of UMP and TCL have witnessed an increase in their shareholding in the above time period (though not fully able to make up for the reduction in promoter shareholding due to the selling promoters).

|

|

Disclaimer

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services and as an Investment Advisor. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.